Small- to medium-sized businesses (SMBs) are increasingly facing challenges in accessing the credit they need to run and grow their operations. As rising costs and inflation take a toll, many are turning to external financing options. However, despite the availability of various financing options, a significant portion of SMBs still struggle to access credit, leaving them vulnerable to closure.

In “What’s Next in Credit: Why SMBs Prefer Corporate Credit Cards for Short-Term Financing,” PYMNTS Intelligence drew on insights from a survey of over 1,020 firms generating $10 million or less in annual revenue to examine the challenges SMBs face in accessing credit to support their businesses, as well as explore small businesses’s preference for corporate credit cards for short-term financing.

According to the research study, a Cross River collaboration, only 47% of SMBs generating annual revenues of $10 million or less reported having access to business or personal financing as of July. This limited access to credit is a concern for SMBs across different market sectors, particularly the professional services and personal and consumer services sectors, which are less likely to have access to financing compared to other industries.

To address their financial needs, many SMBs are relying on business cards, specifically corporate credit cards, which has emerged as the most common form of business financing within the SMB landscape. However, access to corporate cards is relatively low across diverse market sectors, with only 28% of smaller SMBs having access to them.

Overcoming challenges such as cost, eligibility criteria, the approval process, and the complex application process remains key to boosting corporate card utilization, the study further found. But despite these hurdles, a promising market opportunity is emerging for card issuers.

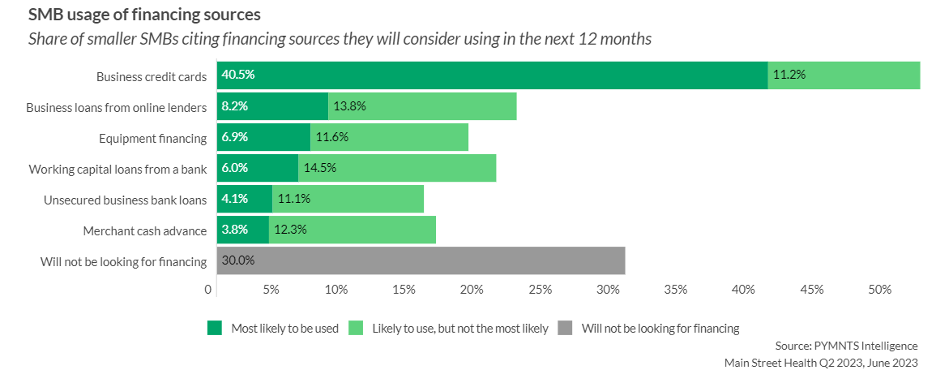

According to the report, a quarter of SMBs plan to increase their use of credit products in the next year, with 52% considering business credit cards as a potential financing source.

One of the benefits of corporate credit cards as a working capital solution for SMBs lies in their ability to cover both anticipated and unforeseen expenses. Among larger SMBs, for instance, more than 90% leverage corporate or virtual credit cards for anticipated costs, while 78% deploy them for unexpected expenditures.

Moreover, corporate cards offer interest-free access to working capital, featuring payment timelines trailing behind spending by 30 to 60 days. This flexibility enables SMBs to carry a revolving balance during periods of tight cash flow. Suppliers, too, benefit from nearly instant access to funds and relevant transaction data, enhancing their accounts payable processes and payment terms.

Despite the evident advantages, however, not all SMBs are turning to external financing in response to inflation and escalating costs. Notably, the study found that 30% of small businesses have no plans to seek financing in the next 12 months. This raises questions about the factors contributing to their financial independence and the alternative strategies they may be employing to sustain and strengthen their operations in the face of economic uncertainties.