As younger and affluent consumers drive the trend, open banking payments stand on the verge of widespread acceptance. This payment method, which allows users to complete transactions directly from their bank accounts using familiar online banking credentials, offers a streamlined alternative to traditional methods by bypassing credit card details.

Yet, despite its advantages, only 11% of U.S. adults have used open banking payments in the past year, even though nearly 46% express strong interest. To unlock this potential, providers must address key barriers such as security concerns, enhance awareness and implement compelling incentives.

The PYMNTS Intelligence report, “Consumer Sentiment About Open Banking Payments,” done in collaboration with Trustly, sheds light on this gap between high interest and low adoption. This gap is primarily due to limited awareness and security concerns, highlighting a significant opportunity for growth if these challenges are addressed.

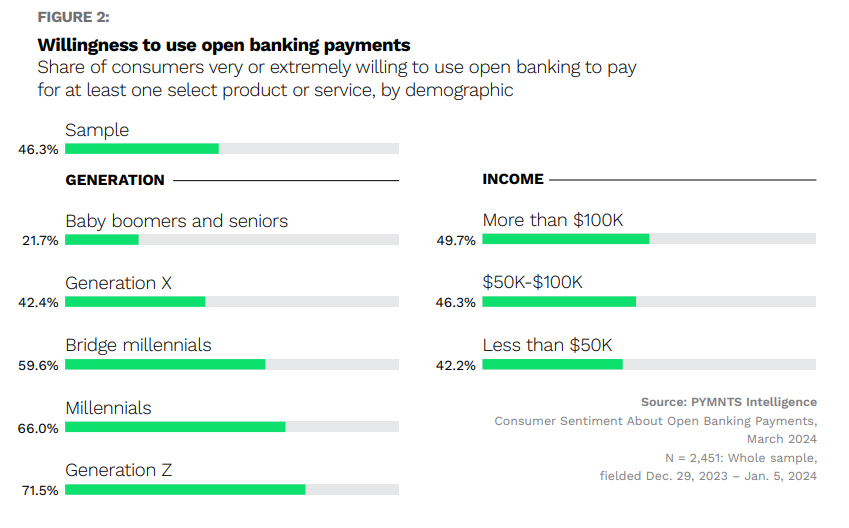

According to PYMNTS Intelligence, 72% of Generation Z and 66% of millennials show high enthusiasm for using open banking payments, significantly outpacing older generations. In contrast, only 42% of Generation X and 22% of baby boomers exhibit similar willingness.

This generational disparity suggests that open banking providers should focus their marketing efforts on younger demographics, who are more inclined to integrate this payment method into their routine transactions. Additionally, high-income individuals are more likely to adopt open banking payments, with 50% of those earning over $100,000 annually expressing interest, compared to 42% among those with lower incomes.

The report reveals that 56% of non-users cite trust issues as a significant barrier, while 44% are unfamiliar with the concept of open banking payments. Security concerns are particularly prevalent among older consumers, with 64% of baby boomers and seniors highlighting this issue, compared to 44% of Gen Z and millennials.

To address these barriers, open banking providers must focus on enhancing security measures, improving transparency and increasing consumer education. Partnering with established financial institutions could also help build trust and credibility.

According to the report, 38% of consumers would be more inclined to use open banking payments if offered discounts, with this figure rising to 52% among millennials and Gen Z. Similarly, 37% of consumers are influenced by loyalty programs, with a stronger preference among younger generations.

By integrating these incentives into their offerings, open banking providers can enhance appeal and encourage wider adoption. As consumers become more familiar with the benefits of open banking, their satisfaction levels rise, particularly among frequent users, with 82% of those using the payment method more than 15 times in the past year expressing high satisfaction.

As a result, this satisfaction increases their likelihood of switching to businesses that support open banking payments, further emphasizing the need for providers to create compelling incentives to drive usage.

To capitalize on the high interest but low current use of open banking payments, providers should focus on increasing awareness and trust while leveraging incentives. Tailoring strategies to highlight the benefits of open banking payments for routine transactions, addressing security concerns transparently and offering attractive incentives will be crucial in bridging the gap between consumer interest and actual adoption.

With the right approach, open banking payments have the potential to become a mainstream payment option, especially among younger and higher income consumers who show the strongest interest and willingness to integrate this innovative payment method into their financial routines.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More